Analysis of Fiji's Economic Performance by Party Leader, Mr. Savenaca Narube

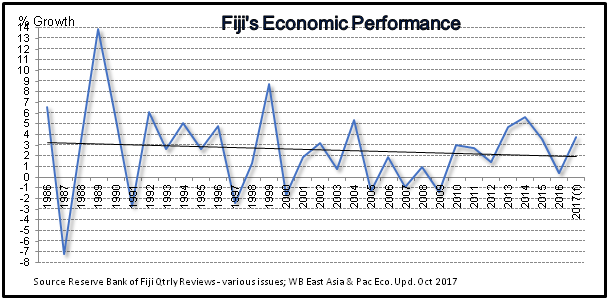

We have heard different interpretations of the performance of Fiji’s economy. What do the facts say? Below is the picture of Fiji’s economic growth since 1986.

Growth is both volatile and declining

Growth volatility arises from two sources. The first are natural disasters like hurricanes and droughts. We cannot control the weather, so these are bound to re-occur in future. The second are the coups. We must put a stop to these and we trust that this Government will keep its promise that we have seen the last of them in 2006.

The volatility in our economic performance strongly suggests that we must create a cushion or, as the recent International Monetary Fund (IMF) Mission puts it, “buffers”, which we can lean on when the bad years hit. This buffer can be a pool of cash which we put aside each year. We do not have this. This buffer can also be in a moderate debt position allowing us room to borrow when we hit an economic crisis. Again, we do not have this. Our debt is already high.

Without this buffer, our economy is extremely vulnerable right now.

Our economy is seriously underperforming

The straight line in the graph is the growth trend over a long period of time. It has continually declined to 2%. This is too low to create enough jobs for our school leavers. It is too low for our income to keep up with inflation. It is too low to provide enough support to the poor.

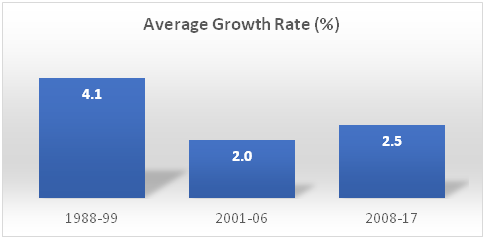

Several studies have calculated that our potential growth rate is about 5%. On average, we are performing at less than half of our potential. The reasons for this under performance have been over analysed by many, but, to me, they boil down to one thing--poor and short-term decision making by politicians.

To lift our long-term growth potential to say 7-8%, we need to do two things. First, we must raise productivity. I have not seen any indicator that productivity has improved. The worsening traffic congestion inflicted upon us by government policies is hurting productivity badly. Second, we need to widen our economic base. We seem to be stuck with tourism. Agriculture which everyone realises is where our potential is, languishes at less than 10% of GDP from a peak of over 20%. No significant new industry has emerged since garment and water in the early 90s.

Our economic base has been stagnant. Our traditional industries are declining. These are serious economic problems.

Our current economic performance is lower than in the past

Due to the long political instability after the 2006 coup, the economy did not start to grow again until 2010. Since then, we have had 8 years of consecutive growth. But the average growth rate from 2008 to 2017 of 2.5 % is well below past performance.

We need to lift our average growth rate to over 4% which we achieved in the 90’s on the back of the garment industry and better performance by our traditional resource sectors. But these traditional resource sectors are dying. Sugar and gold production are far lower than what they used to be.

To double our average growth rate to 4%, we need to dismantle barriers that shackle our economy through innovative solutions and structural reforms. And we need to do it now.

Our current drivers of growth will not last

It gets worse. It is not sufficient to look at the growth rate alone. We must examine what is driving growth. Since 2006, our economy has been propped up largely by injection of millions of dollars by Government from its own operating expenditures like wages and salaries and populist giveaways; and from the withdrawals of members’ funds from the FNPF.

These cash injections are largely spent on consumption and therefore their impact on the economy do not last. To support growth over time, Government will need to continuously pump more money into the economy. A second-year economic student will warn us that this is a very dangerous thing to do. While we enjoy growth as we are doing now, it will not last. We cannot afford to continue to spend at this rate and keep increasing our debt. Ultimately, we will have to reduce spending. This was the reason that the IMF Mission had called for a reduction in operating expenses.

Government is intervening heavily in the private sector

It gets worse. The best way to grow the economy is through the private sector. They, provide more job, earn us valuable foreign exchange, and, most importantly, do not add to our national debt. To develop and grow a dynamic private sector requires that Government leaves them alone to do the things they do best. Tragically, many anecdotes in the last 12 years clearly show that this Government has heavily intervened in the private sector to the extent of picking favourites and sanctioning corporates that do not support them. We will not attract new investors and many of our school leavers will not find jobs in this climate of favouritism and victimisation. Moreover, such a climate multiplies manyfold the risk of corruption.

The World Bank publishes the “Ease of Doing Business” which is a global indicator of how well government supports the private sector. The most recent result shows that Fiji has slipped very badly from being ranked 58 in 2012 to now 101. We are going backwards and must reverse this deteriorating trend.

We must shift the driver of the economy from government to the private sector by creating a level playing field, reducing the heavy handedness of government intervention and introducing policies that promote private sector development.

We need a responsive economic manager now

In summary, our economy is seriously underperforming due to poor economic management. Performances since 2006 have been propped up by measures that are aimed to please the voters but will not last. We do not have a financial cushion to tidy us over when a bad patch comes our way. Government is not managing our debt wisely to give us borrowing room in the future when we need it. Our resource sectors are declining. No new industry has emerged. By playing favourites in the private sector and sanctioning those that do not support them, the government is seriously denying our youths employment.

Our economic problems call for innovative and structural solutions which, unfortunately, have yet to emerge. In my view, we urgently need a responsive economic manager that:

- looks at the long term rather than just short-term populist measures;

- build financial buffers by cutting back on unnecessary and wasteful expenditures;

- moderate the level of debt through reduction in spending;

- allow the private sector to provide more jobs by limiting the role of government to setting standards, promoting policy certainty, and defining the legal boundaries;

- introduce economic reforms to restore the potential of resource sectors, improve productivity and create new industries; and

- better redistribute the benefits of economic growth to the poor through the budget allocation and supportive policies.

These suggestions will ensure that our people, especially the youth and the poor, do not bear the heavy burden of future adjustments that will be forced on them to put the economy back onto an even keel. We must heed the advice of the IMF and learn from actual financial crises in the Pacific and the World.